Industrial Hydrogen Supply Chain Risk: What a Week in Rotterdam and Duisburg Actually Showed Us

The World Hydrogen Summit is where hydrogen ambition is on full display. The site visits are where the gaps become visible. Here is an honest read of both, and what they mean for industrial buyers making hydrogen decisions right now.

There are two versions of the hydrogen industry in 2026. The first is the one you see at a conference like the World Hydrogen Summit in Rotterdam: ambitious, well-funded, and moving fast. The second is the one you see at a Carbon2Chem plant in Duisburg, or walking a hydrogen terminal at the Port of Rotterdam. It is more complicated, and considerably more instructive.

HYDGEN's EVP of Business Development, Arjun Mehta, participated in two panel sessions at WHS 2026 as part of India's official delegation. We also spent time at thyssenkrupp nucera's Carbon2Chem facility, Port of Duisburg, and the Port of Rotterdam in the days before the summit opened. This piece is not a recap of those events. It is an attempt to say something useful about what we observed, particularly for industrial companies trying to navigate the hydrogen transition with real operational constraints in front of them.

The infrastructure ambition is real. So is the delivery gap.

Industrial hydrogen supply chain risk is not a fringe concern in 2026, it is a mainstream procurement issue. The question is how widely it has been internalised.

At the Carbon2Chem facility in Duisburg, the story is one of genuine engineering achievement operating within real structural constraint. The plant works. Electrolysis is integrated into an industrial process at scale. But what is being demonstrated is a proof point — it has not yet been replicated across European industry at the pace that roadmaps imply.

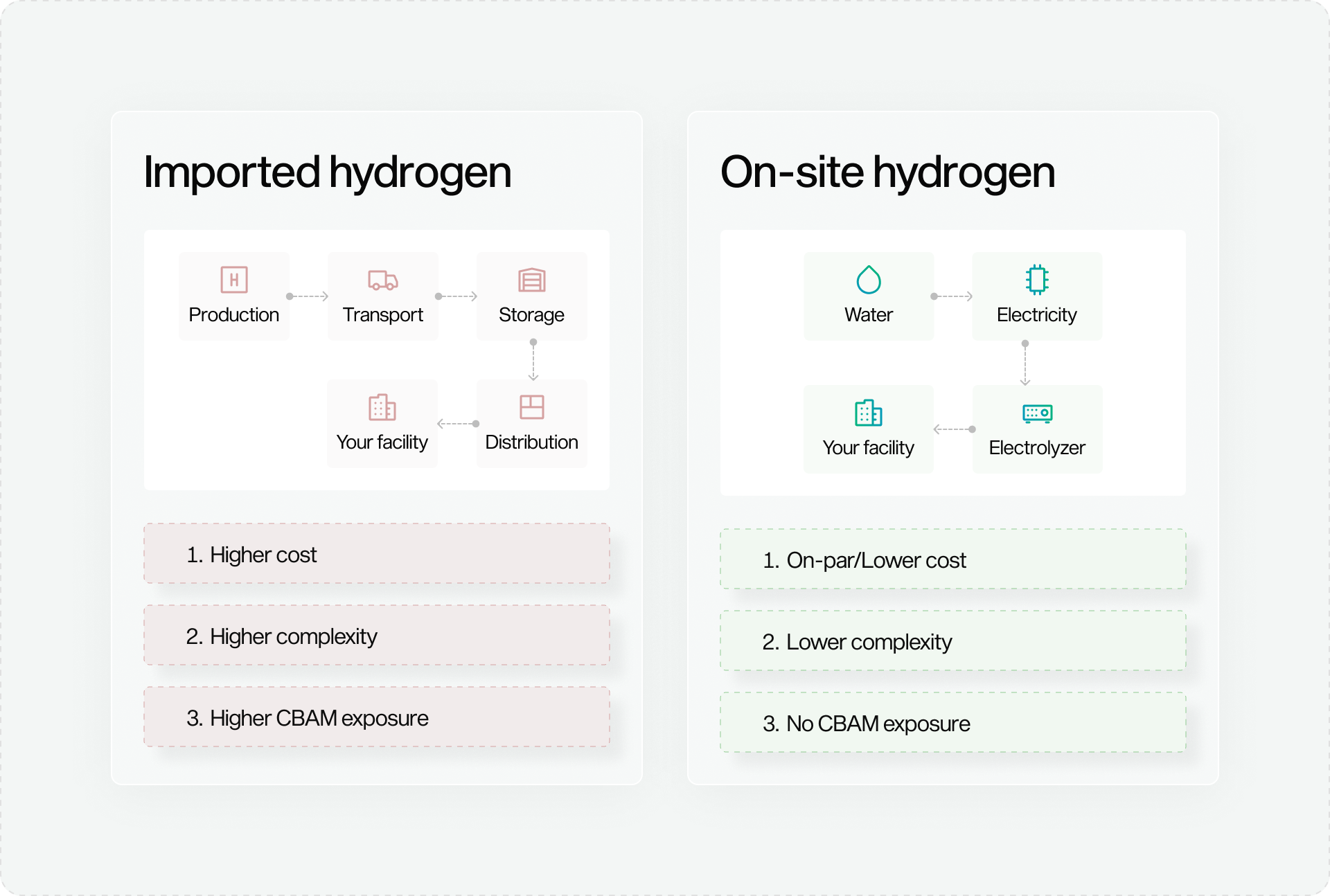

The Port of Rotterdam makes the same point at a different scale. Hydrogen pipeline corridors are being built. Ammonia import terminals are in development. The infrastructure is being designed for supply that does not yet exist at the required volume. This creates a structural vulnerability for any industrial operation that plans its hydrogen strategy around that infrastructure being ready on schedule.

On-site hydrogen generation - producing hydrogen directly from water and electricity at the facility where it is consumed - eliminates this exposure by design. There is no supply chain to fail. This is the core operational argument for decentralised electrolysis, and it is distinct from the green credentials argument that dominates most conference conversations.

CBAM is repricing hydrogen supply chain decisions right now

The Carbon Border Adjustment Mechanism is no longer theoretical. Q1 2026 CBAM certificate prices settled at approximately €75 per tonne, and the impact on European ammonia imports is already visible, volumes down roughly 50% from peak, with per-tonne charges ranging between USD 60 and USD 200 depending on origin and production pathway.

For industrial companies sourcing hydrogen through traded supply chains, CBAM introduces a carbon liability that is now measurable and growing. On-site hydrogen generation, where the production footprint is controlled and auditable at the facility level, eliminates this liability structurally. The commercial logic is simple: a supply chain that does not exist cannot be taxed.

This is not a marginal efficiency argument. For manufacturers in specialty chemicals, advanced materials, and fertilisers, the procurement decision on hydrogen is increasingly inseparable from the compliance decision. Rotterdam was the first major conference where this was discussed with genuine commercial specificity rather than policy abstraction.

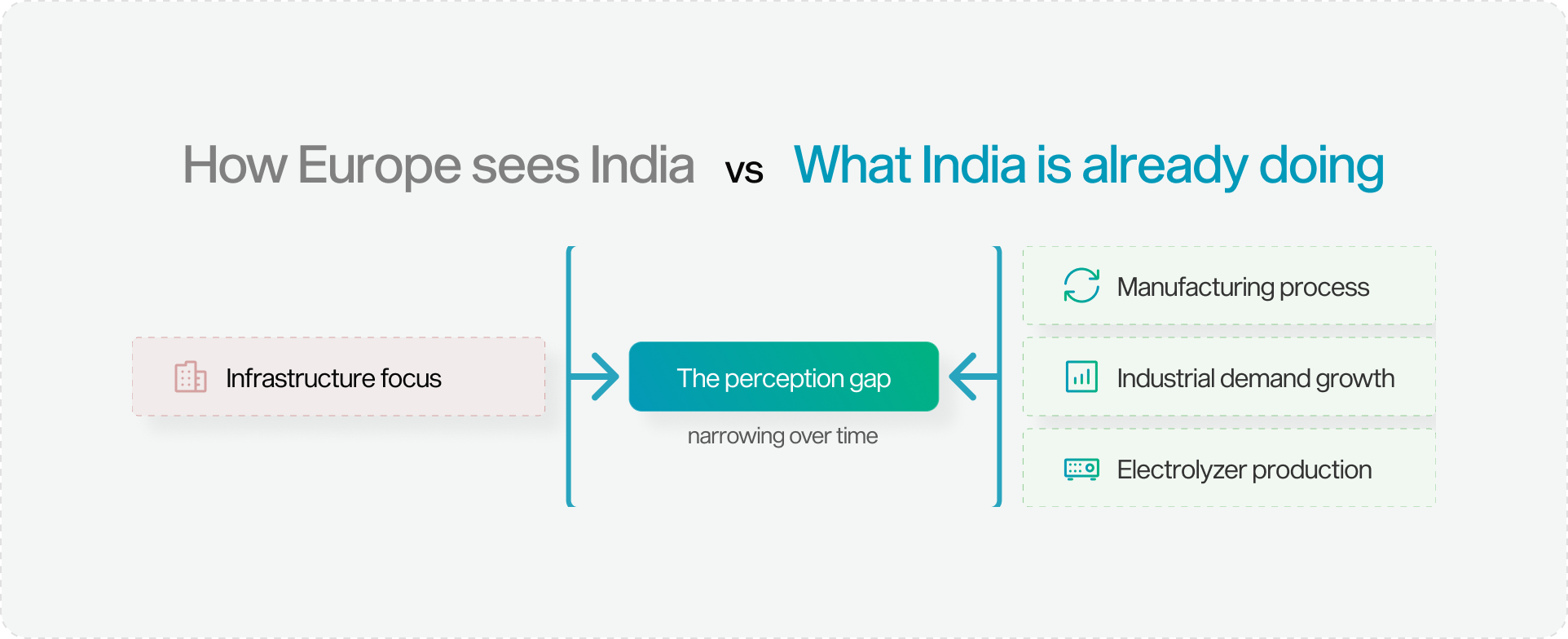

The India dimension is being underestimated

India's official hydrogen delegation at WHS 2026 - organised through MNRE, SECI, IGCC, and CII - was one of the more substantive national presences at the summit. The sessions on scaling bankable hydrogen and ammonia projects and the EU-India Green Hydrogen Dialogue both produced conversations that were more commercially grounded than typical conference fare.

What was striking was the asymmetry between how European players are thinking about India and how India is already operating. Indian industrial hydrogen demand is substantial, growing, and concentrated in sectors - specialty chemicals, advanced materials, electronics manufacturing - that are expanding faster than most European market models assume. Indian electrolyser manufacturing capability is further along than the mainstream European conversation acknowledges.

For companies positioned on the on-site generation side of the value chain, this asymmetry is a commercial opportunity. The perception gap between what India is doing and what it is believed to be doing narrows over time. Being in that conversation early matters.

Where precision industrial users fit, and why they are not waiting

The dominant narrative at WHS 2026, as at most hydrogen conferences, skewed toward large-scale infrastructure. This is appropriate for the questions it is addressing. It is not, however, the whole picture.

There is a category of industrial hydrogen user - CVD diamond manufacturers, semiconductor fabs, specialty chemical facilities - for whom the infrastructure timeline is irrelevant. Their hydrogen requirements are too specific, their purity specifications too demanding, and their tolerance for supply interruption too low for the centralised supply chain to serve them well even when it is fully built.

For these users, the industrial hydrogen supply chain risk calculation is already settled. On-site generation is the answer. The remaining questions are engineering ones: system reliability, flow rate adequacy, facility integration. Those questions are being answered in deployed systems, not roadmaps.